Our new Digital 2021 October Global Statshot Report – published in partnership with We Are Social and Hootsuite – is packed with impressive milestones.

The top headline this quarter is that social media users have passed the 4½ billion mark, but there are also big new numbers for Internet users in China, TikTok’s active user base, and Facebook’s advertising audience.

We’ve also got insights into podcast use around the world, the growing popularity of VPNs, and a look ahead to some of the most important trends that will shape marketing success as we head into 2022.

Essential headlines

You’ll find a handy summary of this quarter’s top stories in the video embed below (click here if that’s not working for you), but read on below for the full report, and for my in-depth analysis of the latest essential trends.

Just before we dive into the data, I’d like to say a big thank you to the partners who make our Global Digital Reports possible: GWI, Statista, Semrush, Skai, SimilarWeb, Locowise, and App Annie.

Full report

The SlideShare embed below contains the complete Digital 2021 October Global Statshot Report report (click here if that’s not working for you), but read on past that to understand what all these numbers mean for you.

The ‘state of digital’ in October 2021

Let’s start with a look at the essential headlines for digital use around the world today:

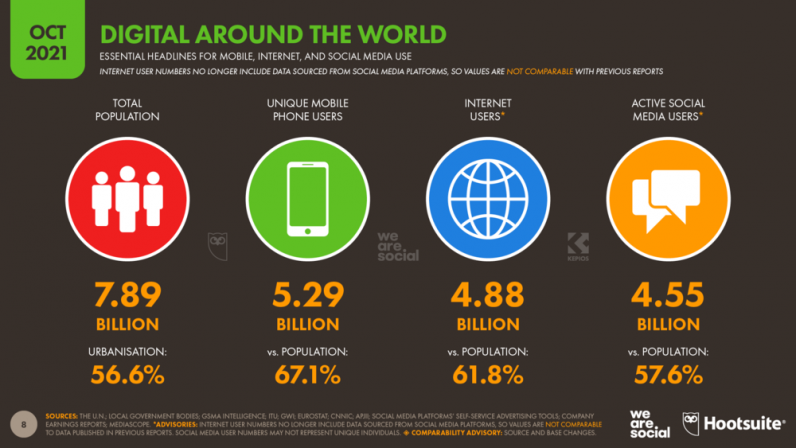

- More than two-thirds of the world’s population uses a mobile phone today, with global users increasing by almost 100 million (+1.9 percent) over the past 12 months to reach 5.29 billion in October 2021.

- There are now 4.88 billion internet users around the world, which equates to almost 62 percent of the world’s population. The latest data show that global internet user numbers have increased by more than 220 million (+4.8 percent) over the past year, but with COVID-19 continuing to hamper research, the real figure may be considerably higher.

- Social media users increased by more than 400 million (+9.9 percent) over the past 12 months to reach 4.55 billion in October 2021. User growth has slowed slightly over the past 3 months, but the global total continues to increase at a rate of more than 1 million new users every single day.

- For context, the world’s population reached 7.89 billion at the start of October 2021, representing an increase of roughly 80 million people (+1 percent) compared with this time last year. Current growth rates indicate that the global population will exceed 8 billion by mid-2023.

Let’s dig deeper into this quarter’s report to learn more.

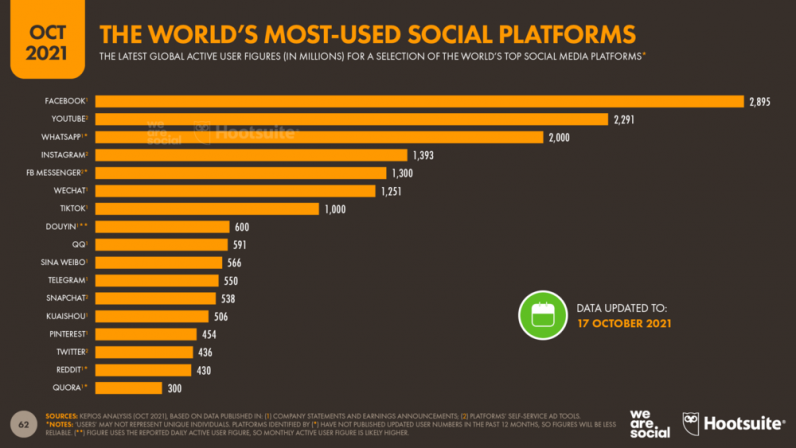

Social media users reach another impressive milestone

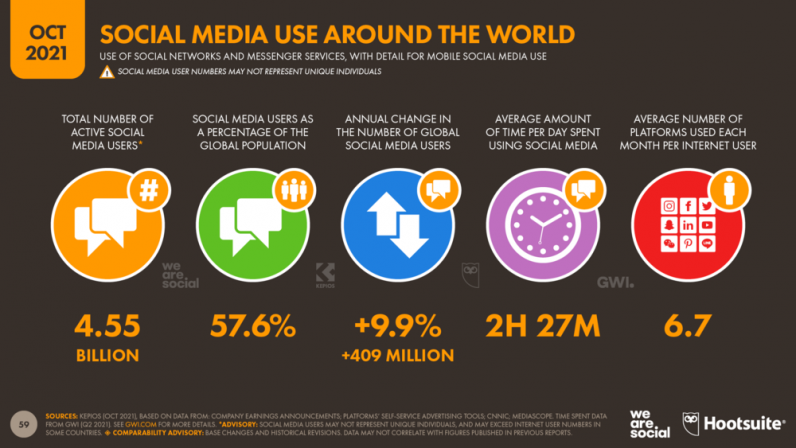

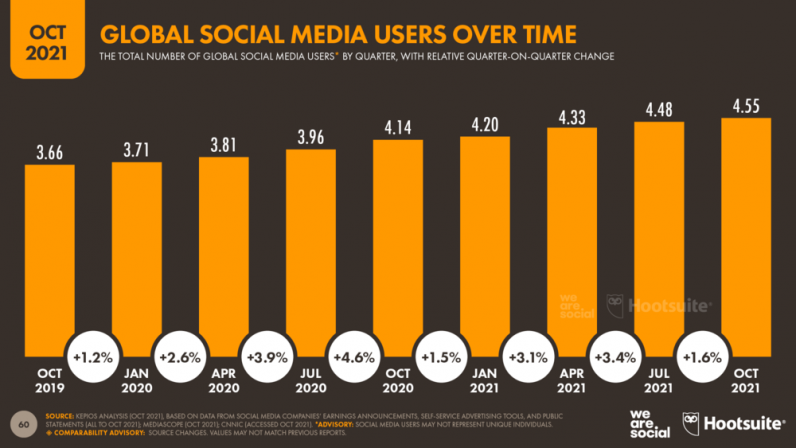

The top story in this quarter’s report is that there are now more than 4½ billion social media users around the world.

That figure is more than 400 million higher than it was this time last year, equating to year-on-year growth of almost 10 percent.

Social media user numbers are still growing steadily too, with an average of 13 new users starting to use social media for the first time every single second.

User growth has slowed slightly compared to the annual growth figures we reported in our April and July Statshot reports, but the latest figure is still higher than the growth rate we reported in our last pre-COVID report in January 2020.

It’s also worth stressing that we’ve been anticipating ‘less rapid’ growth for some time now, and it’s actually taken a couple of quarters longer than we expected for growth rates to return towards their pre-COVID pace.

However, even at this ‘slower’ pace of growth, current trends suggest that social media users will still pass the equivalent of 60 percent of the world’s total population some time in the first half of 2022.

China is now home to more than 1 billion internet users

The latest report from CNNIC reveals that over 1 billion people in China now use the internet, accounting for more than 1 in 5 of the world’s total internet user base.

More than 70 million people in China started using the internet over the past year, resulting in year-on-year growth of 7½ percent – well ahead of the global average growth rate of 4.8 percent.

This figure means that China accounted for almost one-third of the 222 million new users we’ve added to our global user total since this time last year.

Roughly 70 percent of China’s total population is now online – up from 65 percent this time last year – while 2 new users join their ranks every second.

However, there’s still plenty more room for growth, with CNNIC’s data indicating that more than 400 million people across the country are yet to come online.

TikTok passes the 1 billion user mark

TikTok announced that it had passed the 1 billion monthly active user figure at the end of September 2021, making it just the seventh social media platform to join the exclusive billion-user club.

What’s more, TikTok has reached this impressive figure despite being still blocked in India – a country that is home to more than 650 million internet users, or roughly 15 percent of the global internet population.

TikTok’s user growth shows few signs of slowing either, with App Annie reporting that the platform continued to top global download rankings for non-game apps between July and September this year.

For a platform to reach that same share of social media users today, it would need to attract roughly 2 billion monthly active users.

Regardless of comparative growth rates, however, there’s no denying that 1 billion active users is enough to make any marketer sit up and take notice.

But just how compelling is the TikTok marketing opportunity?

Well, the good news is that we’re (finally!) able to report detailed figures for TikTok advertising reach around the world in this quarter’s report.

TikTok: the advertising opportunity

Just before we dig into the detailed stats for TikTok’s advertising audience, please take careful note of the following:

- The potential advertising reach figures we’ve included in this quarter’s reports come from TikTok’s self-service advertising tools. These tools publish potential reach as a range (e.g. 18,000-20,000), and we use the midpoint of that range (e.g. 19,000) for our published reach figure.

- TikTok’s self-service advertising tools only publish audience reach data for users aged 18 and above, even though the same tools allow advertisers to target adverts to users aged 13 and above. As a result, the figures that Bytedance reports in these tools may be significantly lower than TikTok’s total active user base, as well as its total potential advertising reach.

- The company’s tools only publish potential reach data for a selection of countries, and as a result, figures published in these tools may not reflect the platform’s total global advertising audience. In particular, note that TikTok’s self-service advertising tools do not report data for Douyin in China, which ByteDance operates as a separate platform.

- Comparisons to population (e.g. percentage of population aged 18 and above) are based on the latest population data from the United Nations and the US Census Bureau (note that the US Census Bureau publishes population data for a wide variety of countries, not just the United States). However, as is the case for all social media platforms, age-related figures may be skewed by users misrepresenting their age on TikTok.

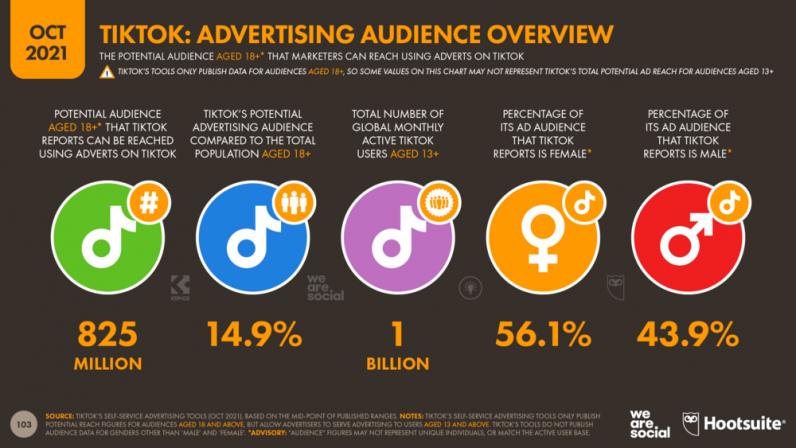

With those caveats in mind, ByteDance’s latest numbers indicate that marketers can now reach 825 million users aged 18 and above around the world via ads on TikTok.

For context, those figures suggest that TikTok ads now enable marketers to reach:

- 10 percent of the world’s total population, regardless of age or location

- 15 percent of everybody aged 18 and above, regardless of location

- 24 percent of everybody aged 18 and above outside of China (which has a separate app) and India (where TikTok is currently unavailable)

However, as we see in the data for all other platforms, TikTok’s reach varies considerably by geography and by demographic.

The TikTok audience by gender

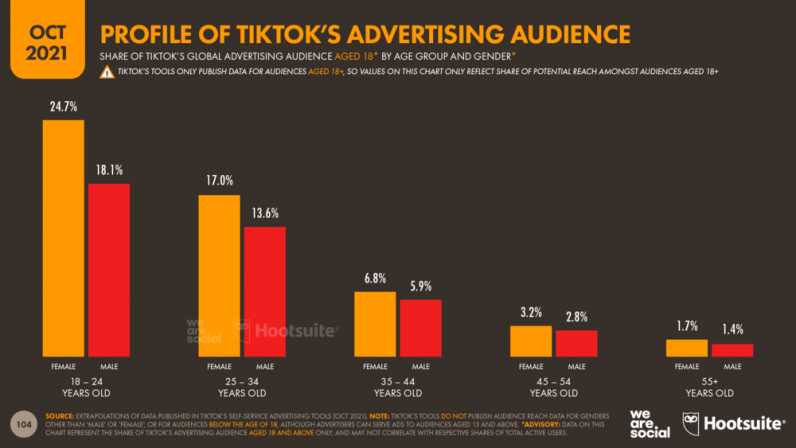

For example, the company’s own data indicates that 56.1 percent of the worldwide TikTok ad audience is female.

Interestingly, this represents a ‘flip’ of Facebook’s gender ratio, where male users account for 56.5 percent of the global advertising audience.

However, it’s worth highlighting that Facebook’s gender ratio is somewhat skewed by its audience demographics in India, where men account for more than 75 percent of the platform’s 350 million monthly active users.

Note: TikTok doesn’t report audience data for genders other than ‘female’ or ‘male’, which is why we’re only able to report binary gender splits.

The TikTok audience by age

As noted above, ByteDance’s tools only report data for TikTok users aged 18 and above, so we’re currently unable to report potential advertising reach for users between the ages of 13 and 17.

However, the available data clearly supports the hypothesis that TikTok is particularly popular amongst younger users.

Specifically, users aged 18 to 24 account for roughly 45 percent of TikTok’s global ad reach amongst users aged 18 and above.

What’s more, women in this age group account for roughly a quarter of the platform’s total advertising audience aged 18 and above.

For context, that means women aged 18 to 24 account for a greater share of TikTok’s advertising audience than users of any gender aged 35 and above do.

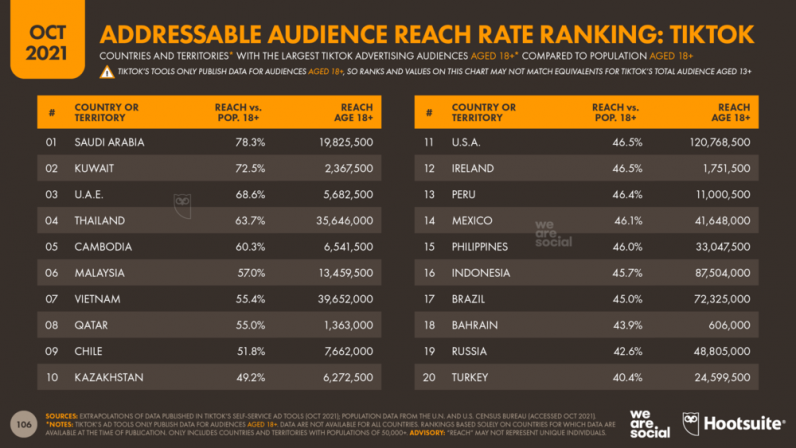

TikTok’s biggest advertising markets

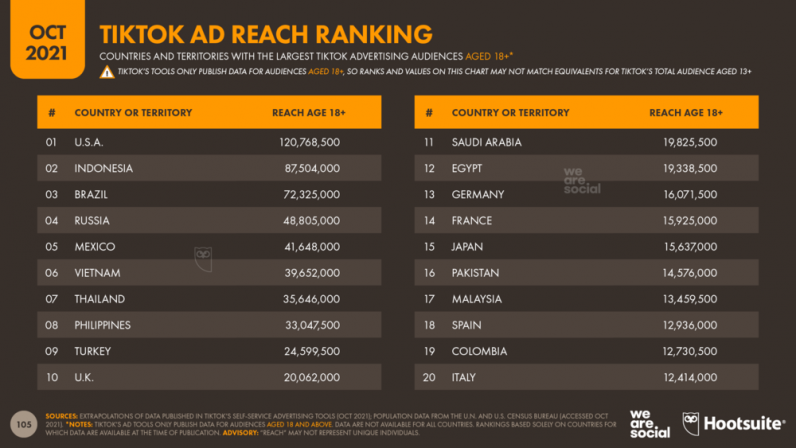

The United States is home to TikTok’s largest advertising audience, with the latest data showing that TikTok ads now reach more than 120 million US users aged 18 and above.

For reference, that’s just 20 percent lower than the 150 million American users aged 18 and above that marketers can reach using ads on Instagram.

It’s also interesting to note that TikTok’s US ad reach figure is equal to 46.5 percent of the total US population in the same age range, although younger users misrepresenting their age may somewhat skew this ratio.

Indonesia claims second place in TikTok’s ad reach ranking, with the company’s tools reporting a potential reach of more than 87.5 million Indonesian users aged 18 and above.

Brazil comes in third, with more than 72 million users in the same age group.

For example, TikTok appears to be particularly popular in the Middle East.

The number of TikTok users in Saudi Arabia is equal to nearly 80 percent of the country’s total population aged 18 and above, and the platform’s local user base is already significantly larger than that of either Facebook or Instagram.

TikTok has also developed a strong user base in Kuwait and the UAE, where the platform’s ad products offer potential reach equivalent to more than two-thirds of all adults aged 18 and above.

The platform is also very popular across South-East Asia, with TikTok’s ad reach figures equal to more than 6 in 10 adults aged 18 and above in Thailand and Cambodia, and more than half of that age group in Vietnam and Malaysia.

However, TikTok isn’t alone in posting impressive ad reach figures this quarter.

Potential ad reach across Facebook Inc.’s platforms now exceeds 3 billion

The latest numbers reported in Facebook’s self-service tools indicate that the company’s portfolio of platforms now enables advertisers to reach a combined potential audience of more than 3 billion distinct users.

That might not sound like ‘news’, because Facebook Inc.’s investor earnings reports indicate that the company’s Family Monthly Active People (FMAP) figure exceeded 3 billion in Q2 2020.

However, that FMAP figure also includes WhatsApp’s 2 billion-plus users, and WhatsApp doesn’t currently offer advertising placements.

Furthermore, our analysis suggests that total potential advertising reach on Facebook only equates to about 78 percent of the platform’s monthly active users (note that this is specific to the Facebook platform, and not the company’s overall portfolio of platforms; click here for a more detailed analysis).

Based on the above, this is the first time that Facebook’s tools have reported a combined advertising audience in excess of 3 billion.

These figures suggest that marketers can now reach more than 60 percent of all adults aged 13 and above outside of China using ads on Facebook’s portfolio of platforms.

The company notes that – despite its efforts to ‘de-duplicate’ reach across platforms – there may still be some undetected ‘double-counting’ of audiences across different platforms, while ‘fake’ accounts may also account for a small percentage of total figures.

However, based on the figures for potential audience duplication and fake accounts that the company has cited in documentation such as its investor earnings announcements, advertising on Facebook Inc.’s portfolio of platforms should still reach roughly half of all the world’s population aged 13 and above outside of China.

For context, the latest data published in the company’s own self-service advertising tools indicate that:

- Facebook offers total potential advertising reach of 2.28 billion

- Instagram offers total potential advertising reach of 1.39 billion

- Facebook Messenger offers total potential advertising reach of 1.09 billion

These numbers show that there’s plenty of identifiable overlap in the audiences of each platform, which is separate from the undetected double-counting described above.

However, the company’s data suggests that more than 600 million active Instagram users do not use Facebook, which highlights the value of Facebook Inc.’s portfolio approach.

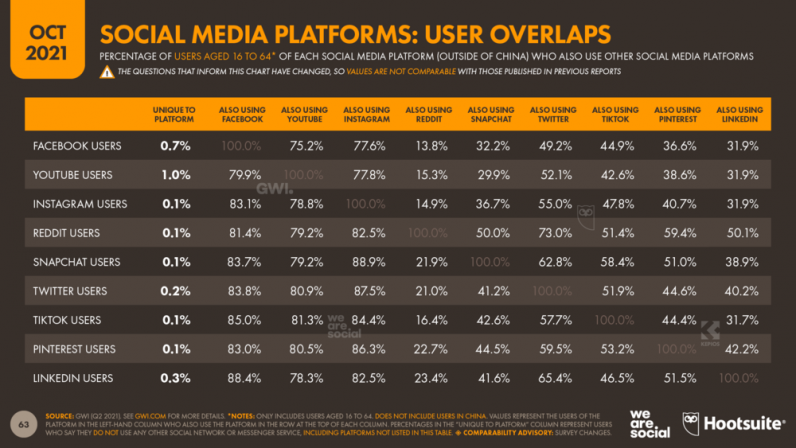

GWI’s latest data tells a slightly different story, with a greater degree of overlap across platforms.

However, it’s worth noting that GWI’s data focuses on internet users aged 16 to 64 in a selection of the world’s larger economies.

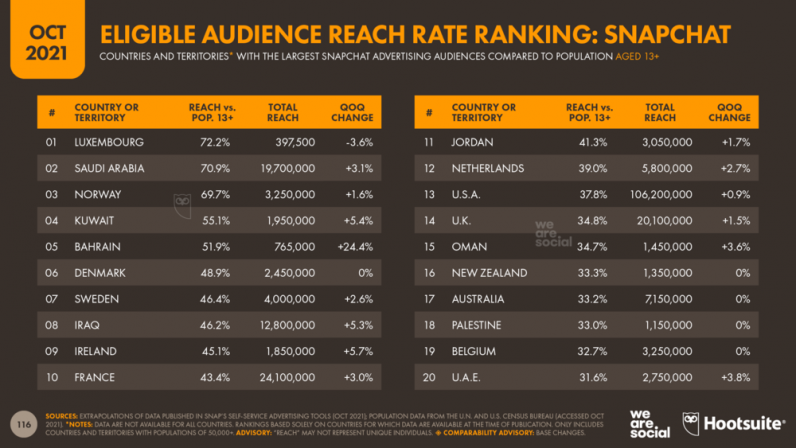

India becomes Snapchat’s top ad audience

The number of users in India that advertisers can reach using ads on Snapchat has surged by more than 16 percent over the past three months.

India has now overtaken the United States to claim the top spot in the ranking of Snapchat’s advertising markets, even though the platform’s reach in the US also continues to increase.

Marketers can now reach almost 116 million users in India via ads on Snapchat, compared with 106 million users in the United States.

India now accounts for more than 21 percent of Snapchat’s total worldwide ad audience, and almost 29 percent of the platform’s global male audience.

Interestingly, male users account for nearly 60 percent of Snapchat’s ad audience in India, compared with a global male average of just under 45 percent.

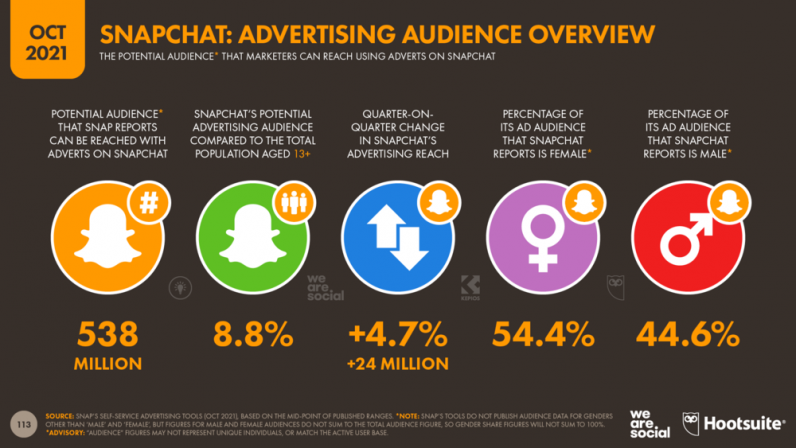

Snapchat has delivered healthy growth in global advertising reach over the past quarter too, adding 24 million new users since our Digital 2021 July Global Statshot Report to take the platform’s total global ad reach to 538 million.

In terms of ad reach compared with eligible populations aged 13 and above, Snapchat appears to be particularly popular with audiences in the Middle East and Scandinavia.

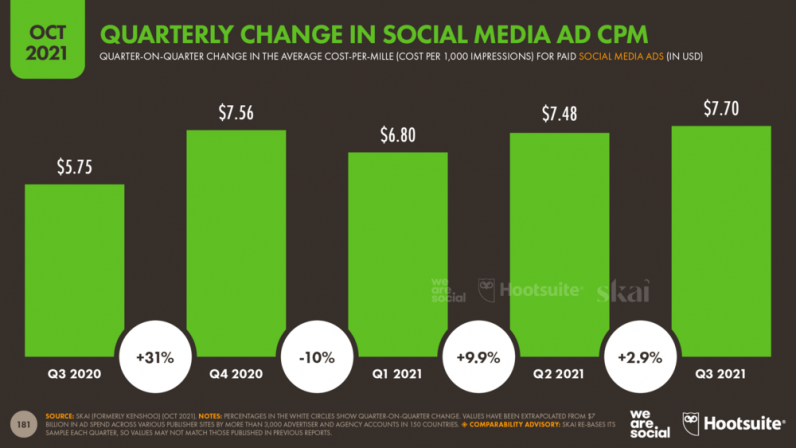

The cost of digital ads jumps

The latest data from Skai (formerly Kenshoo) reveals that the cost of reaching audiences on social media has increased significantly over the past 12 months.

The company’s latest Digital Marketing Quarterly Trends Report reveals that the average global CPM (cost per thousand impressions) has increased by more than 33 percent since this time last year.

For context, Q4 2020 CPMs were 31 percent higher than Q3 2020 values.

Past performance isn’t always a reliable indicator of future trends of course, but if we were to see a similar trend this year, marketers shouldn’t be surprised to see average social media CPMs reach USD $9 for the last 3 months of 2021.

ADVERTISEMENT

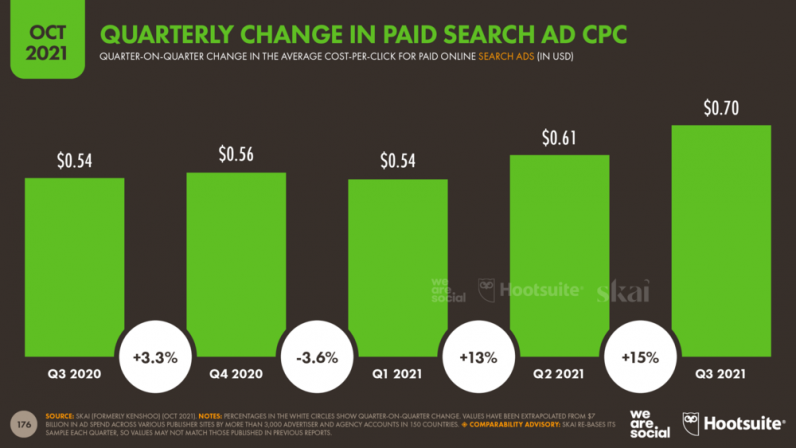

A similar pattern of ad cost inflation is evident in search advertising too, with Skai reporting a 30 percent year-on-year increase in the average global search cost per click (CPC).

Similar to the latest social media trends, search CPCs in Q3 2021 were already well above the average CPC in 2020’s ‘holiday’ quarter (Q4), suggesting we may see even higher costs associated with search advertising over the coming months.

Spend on search ads still increased though, with the latest data indicating a 32 percent year-on-year increase in the total global spend on search advertising.

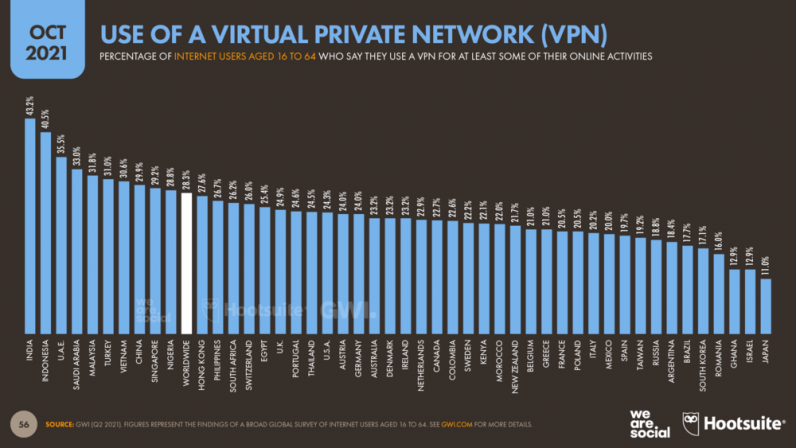

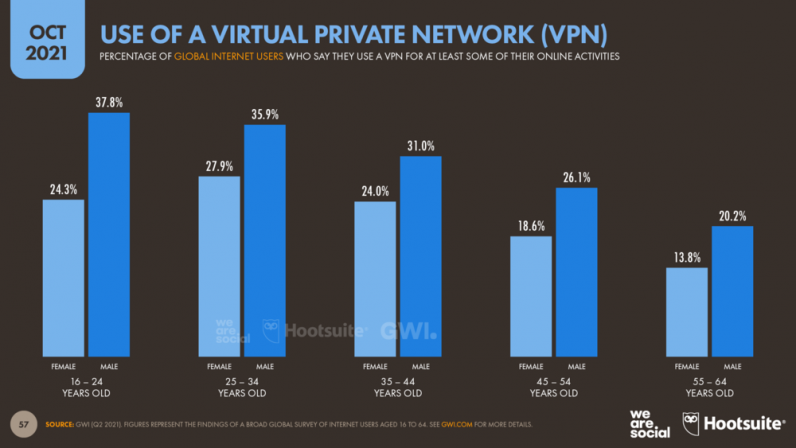

Increasing use of VPNs

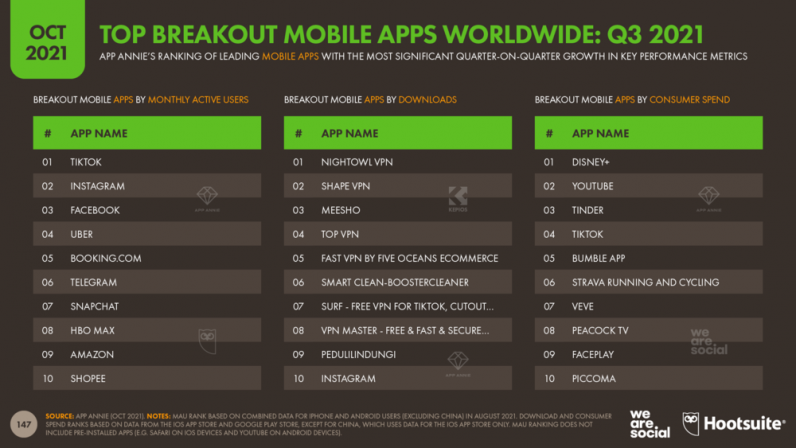

Data from App Annie shows that virtual private networks (VPNs) were the ‘breakout’ story in global app downloads in Q3, accounting for 6 of the top 10 non-game apps with the most significant increase in worldwide downloads between July and September 2021.

Internet users in South and Southeast Asia are the most likely to make use of VPNs, with more than 4 in 10 working-age internet users in India and Indonesia saying they use these tools at least some of the time.

However, there doesn’t appear to be any meaningful correlation between broader privacy fears and the use of VPNs.

GWI’s latest data reveals that roughly one-third of all male internet users aged 16 to 64 already use VPNs, compared to less than a quarter of their female peers.

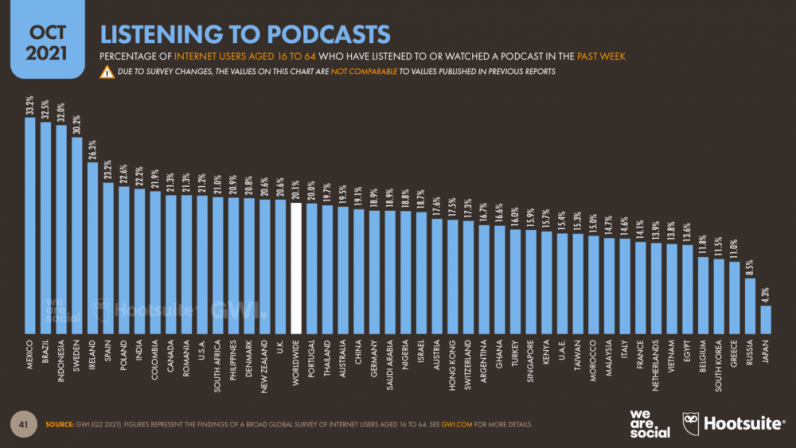

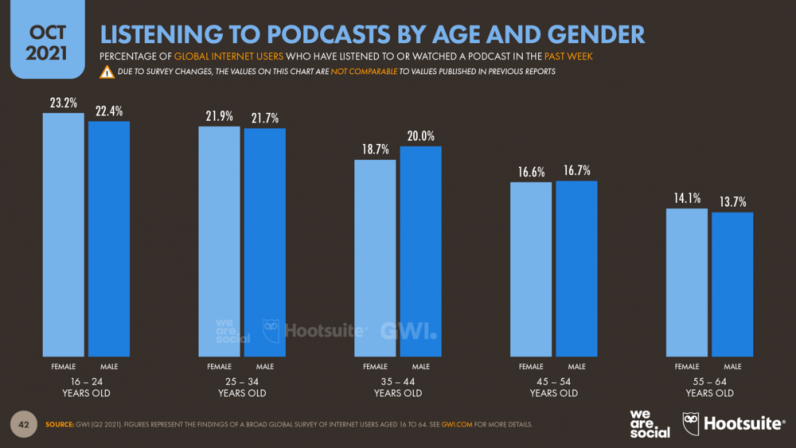

Podcasts growing in popularity

The latest research from GWI shows that more than 1 in 5 internet users aged 16 to 64 around the world now listens to a podcast each week.

However, this figure rises to roughly 1 in 3 amongst the same demographic in Mexico, Brazil, and Indonesia.

However, roughly 1 in 7 internet users aged 55 to 64 also listened to at least one podcast in the past 7 days.

Looking ahead: the outlook for 2022

Over the next few weeks, you can look forward to a whole host of 2022 trends reports from some of the world’s top futurists.

Many of those reports will likely focus on areas like NFTs, the metaverse, artificial intelligence, and cybersecurity, so – rather than repeat those same themes here – I thought it might be more helpful to look at some of the more immediate and more actionable trends that we’ve been tracking in our Global Digital Reports.

Amongst these trends, there are two that I think all marketers will want to explore in more detail:

1. Cross-cultural content

New tools and new platforms have significantly increased the range of content that’s available and accessible to the world’s internet users.

At the most basic level, the improved availability, accuracy, and sophistication of online translation tools mean that it’s never been easier for people to access content that was written in languages other than their own native tongue.

These tools are becoming more popular too, with various trends in our reports showing a steady rise in the number of people who translate text content online.

Meanwhile, TikTok’s content-focused algorithm means that the platform’s billion-plus users now have significantly more chance of being exposed to content created by someone on the other side of the world than they would have had on platforms where algorithms prioritize a user’s social graph.

Similarly, the surge in popularity of ‘international’ TV shows like Squid Game, Money Heist, and Lupin, means that ‘cultural borders’ are becoming increasingly blurred.

Furthermore, with Netflix announcing that it will increase investments in ‘local’ content intended for global audiences, and with TikTok reaching an ever larger global audience, we can expect that blurring to accelerate in 2022.

This trend has critical implications for marketers and content creators everywhere, so click here to learn more about this trend and what it might mean for you.

2. The evolution of search and brand discovery

The world’s online search behaviors are becoming ever more diverse and fragmented.

The use of voice search continues to increase, especially amongst smartphone users in low- and middle-income countries.

Similarly, the use of image recognition tools has already become an essential consideration for marketers in many parts of the world, especially across Latin America and Southeast Asia.

Meanwhile, nearly three-quarters of internet users aged 16 to 64 say that they turn to social media when researching products and services that they’re thinking of buying, making ‘social search’ one of 2022’s top opportunities.

Given the importance of brand discovery and research for marketers, we’ve produced a complete guide to these evolving search behaviors, and their potential implications for brands.

You can read that guide in full – and for free – by clicking here.

In addition to those two essential trends, marketers may also want to explore the themes outlined below.

These themes aren’t projections or forecasts per se; rather, they’re intended to be provocations that inspire more focused thinking, as well as some new ideas.

3. Cross-border ecommerce

People are increasingly looking beyond national borders to find the perfect product, especially when small domestic markets mean that local choices are limited.

Amazon is already making it easier for customers to shop in its other country ‘stores’, and is increasingly offering competitive global delivery too.

Meanwhile, ecommerce platform players like Shopify and Magento are making it easier for independent retailers to engage and serve overseas shoppers.

However, it’s the impact of cross-cultural content – as described above – that will likely play the biggest role in accelerating shoppers’ interest in cross-border commerce in 2022.

Cross-border commerce has its challenges though, from basic issues like language barriers and cultural references, to logistics issues like the speed of delivery and the cost of returns.

4. Shopping as an experience

Online shopping platforms in the West have become masters of ‘checkout efficiency’, but the rise of live-stream shopping formats in Asia demonstrates that there are other successful approaches to ecommerce.

As competition increases in the online shopping world, we can expect to see ecommerce players experiment with new formats that emphasize areas such as social interaction, shopper entertainment, and even augmented services like education (e.g. ‘how-to’ content).

5. Regulation and corporate activism

Regulation is already one of the hottest topics in digital, but we can expect legal and ethical considerations to have even greater bearing in 2022.

On the one hand, governments are putting digital giants under increasing pressure, from China’s emphasis on ‘common prosperity’, to America’s push to mitigate foreign interference and mental health risks, and the EU’s action on competition and taxation.

Increased activism won’t be restricted to governments either; we can also expect to see other companies join Apple and Google in taking proactive steps to protect user privacy and safety.

This may make it seem like there’s more complexity ahead, but my top tip is to embrace these changes.

Proactivity in the areas of consumer safety and privacy will help you to define the best agenda for your business (rather than being reactive), and proactivity should also position you as a more trustworthy brand amongst your customers.

6. The next big disruptor

Entertainment, communication, and retail were the first industries to experience ‘comprehensive’ digital disruption, and various other industries are currently undergoing significant digital transformation.

However, while no industry has escaped digital’s influence, it seems that large-scale disruption has yet to impact three critical categories: education, healthcare, and consumer finance.

It’s true that COVID has accelerated movement in all of these categories – particularly education – but we can expect to see digital disruption accelerate in these industries in 2022, particularly now that COVID has helped us to overcome some of the initial barriers and inertia.

7. Cybersecurity

Various reports have indicated that cybercrime has increased significantly in the past couple of years.

As a result, digital literacy and online safety will become increasingly important for individuals, as well as for the governments that look to protect them.

However, the most worrying cybersecurity threats go well beyond the individual, and – sadly – we can expect to see increased cyber attacks on companies, sovereign nations, and even ideologies in the coming months.

8. Disruptive interfaces

I seem to raise this topic every year, but I’m more convinced than ever that we’re overdue a ‘disruptive’ innovation in the interfaces that we use to engage with our connected devices.

The most obvious candidate is some form of augmented, ‘heads-up’ display – most likely in the form of AR glasses – with Facebook and Apple both tipped to be launching new products ‘imminently’.

However, in the longer-term, direct-to-brain interfaces may completely remove the need for physical devices, enabling users to augment their thinking and perceive physical sensations directly through the stimulation of their brain, nervous system, and hormone receptors.

9. From destination to integration

A move away from screen-based interfaces would help to inspire and promote a wider range of more integrated uses of connected technology.

For context, most of today’s digital products and services are standalone ‘destinations’: we still need to ‘visit’ Facebook, Amazon, Netflix, etc., and – for the most part – they dominate our attention while we use them.

However, the next wave of digital innovation will use connectivity to add an augmented ‘layer’ to other activities, creating new dimensions and adding new value within those experiences, without necessarily becoming their central focus.

In the long run, connectivity will become something akin to electricity: an essential source of power for much of what we do, yet something that we don’t need to think about, because it’s not the core focus of attention.

And for my final provocation this year, an ‘anti-trend’…

10. Beware of squirrels

In the advisory sessions that I run for Kepios’ clients, it’s becoming increasingly clear that many marketers feel overwhelmed by the pace and diversity of digital innovation.

Part of this is self-inflicted, and relates to our industry’s obsession with ‘shiny new objects’ – we’re like Dug the dog from Pixar’s Up!, constantly getting distracted by every passing squirrel.

However, a bigger part of this challenge relates to the sheer scale and breadth of what marketers actually need to know in order to do their jobs, as well as the pressure to experiment and the FOMO that we feel every time a new platform or tool comes along.

But this constant focus on the future may be compromising our ability to perform in the present.

So, while it’s important to keep an eye on what’s next, we perhaps need to spend a bit less time future-gazing, and make better use of what we already have.

Be honest with yourself: what will have a greater impact on your marketing ROI in 2022 – launching an NFT, getting involved in the metaverse, or optimizing the media efficiency of your social media spend?

Yes, NFTs are exciting, but if you’re a marketer, you’ll most likely only be able to use them as a one-off PR stunt. Critically, if NFTs are central to your organization’s future success, it’s unlikely that marketing will be leading the NFT charge.

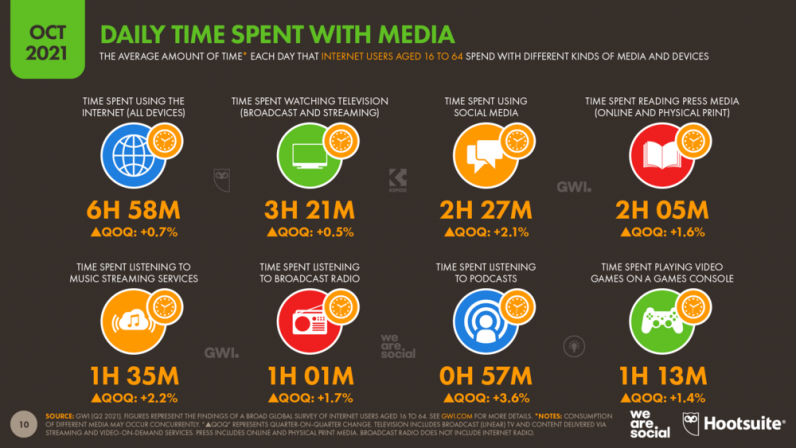

Similarly, the metaverse may well become a ‘place’ where your audience spends an increasing share of its time. However, that’s not going to happen overnight, whereas people already spend 2½ hours a day on social media, and that figure continues to increase.

Don’t get me wrong; NFTs and the metaverse both have plenty of future business potential, but I doubt that either will be the answer to your marketing woes in 2022.

So, do yourself a mental health favor: set aside a couple of hours a month for future-gazing, but focus the majority of your time and attention on the things that will ensure you succeed today.

That’s all for this quarter’s analysis, but I’ll be back in January with our flagship Digital 2022 report.

Get the TNW newsletter

Get the most important tech news in your inbox each week.